The world faces risks ‘both wholly new and eerily familiar,’ the Global Risks Report 2023 warns. Dangers include geoeconomic confrontation, climate change and divisive competition for resources.

The 2023 report from the World Economic Forum ranks risks on a two-year timescale and a longer term 10-year time horizon. It makes for grim reading. The report predicts the next decade will be characterised by environmental and societal crises, driven by geopolitics and economics, with economic warfare normalised, and possibly the first human development rollback in decades.

The report notes that ‘the world is entering a low-growth, low-investment and low-cooperation era’, and that fragmented- and crisis-focused approaches are short-sighted and can perpetuate vicious cycles. It calls for improvements in risk identification and preparedness. It also foresees rising demand for food, water and critical minerals, with continued population growth. It examines resource rivalries too and how emerging risks many combine into ‘polycrises’.

‘It is interesting how frightening and alarmist the report is,’ says metallurgist Antoine Allanore at the Massachusetts Institute of Technology, US. He is disappointed, however, that the report did not propose solutions.

Four futures

The report looked at four hypothetical futures for 2030. The most benign scenario imagines effective climate action and flexible supply chains, ‘enabled by global cooperation’, with shortages in water, metals and minerals. The second scenario foresees resource constraints, with slow climate action and a multi-resource humanitarian crisis in some countries.

But things could be worse. In its ‘resource competition’ future, distrust encourages a push for self-sufficiency in high-income countries. States intervene to secure supplies of critical minerals, which leads to shortages, price wars and disruption to supply. Annual demand for graphite, lithium and cobalt is expected to hit 450% of 2018 production levels by 2050, it noted.

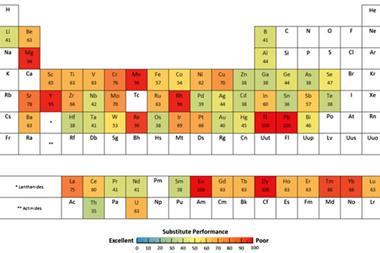

Critical metals are essential for renewable energy and other industries, including technological and military end-users. For instance, indium is needed for touchscreens and solar panels, lithium for pharmaceuticals and cobalt for aerospace applications, as well as green hydrogen production. The EU, for one, is increasingly concerned about sourcing such metals.

There are few options for diversification, according to the report, with the US reliant on imports for 14 critical minerals, including gallium, graphite, indium and vanadium. China accounts for 98%, 82%, 58% and 66%, respectively, of their total production, and is the leading producer of half of 32 strategic minerals.

Demand for resilience fuels stockpiling of resources, which exacerbates supply problems, under this scenario. Other countries could follow Canada’s lead and restrict investments based on national security. Canada recently instructed three Chinese groups to divest their stakes in Canadian mineral companies after a review concluded that their investments in lithium mines posed a threat to national security.

There is also the likelihood of new trading blocs arising, interfering with existing alliances between mineral-rich and -poor countries, ‘while the potential for accidental or intentional conflict escalates’. The importance of alliances will increase too. ‘With a trend towards militarisation, these strategic resources have become one of the primary fronts of economic warfare over the latter half of the decade,’ the report notes.

Worst case scenario

In the fourth scenario, geopolitical dynamics worsen climate-induced food and water shortages, and there are more aggressive clashes between states. Geopolitics converts the natural resource crisis ‘from one of affordability to one of availability, creating a cascading economic, environmental and humanitarian crisis in all but a handful of select countries’.

States would exercise greater control over key resources, thereby fracturing alliances, worsening scarcity and escalating trade tensions that restrict the flow of climate technologies. Conflict across borders becomes more common, as a way of securing the supply of strategy resources.

Allanore agrees that we are seeing the end of globalisation, but he is more optimistic about resource supplies. ‘The report is shy about the discovery of new resources, of local recycling technologies and the development of new technologies for extraction and processing of metals,’ he says.

There can be more regional mining and processing, and the raw materials may cost more, but for many metals there is no paucity of geological reserves or recycling sources. ‘There is a shortage of magnesium in the US, and we don’t have much magnesium production here, but there is an abundance of it in brine, in seawater and dolomite rock deposits,’ Allanore says. Instead, business decisions have pushed almost all magnesium production into Turkey and China.

Vanadium is another example. ‘There are numerous vanadium resources everywhere, but extracting it is an extremely dirty process,’ says Allanore. ‘That’s why it’s mostly processed in Kazakhstan and South Africa.’ Businesses can get hold of these resources, he adds, but it is governments that are especially worried about access, often for military technologies.

Mining and metal processing can also be an unreliable investment. ‘Profitability is not guaranteed and technical risks are high,’ Allanore explains, ‘which is why most western investors would rather invest in cryptocurrencies than ferro–vanadium production in the US.’

No comments yet